StochVolModels

Python implementation of pricing analytics and Monte Carlo simulations for stochastic volatility models including log-normal SV model, Heston

> stochvolmodels package implements pricing analytics and Monte Carlo simulations for valuation of European call and put options and implied volatilities of different stochastic volatility models including Karasinski-Sepp log-normal stochastic volatility model and Heston stochastic volatility model. The project is written primarily in Python, distributed under the MIT License license, first published in 2022. Key topics include: fourier-transform, heston-model, heston-stochastic-volatility, lognormal-stochastic-volatility, monte-carlo-simulation.

🚀 StochVolModels Package: stochvolmodels

stochvolmodels package implements pricing analytics and Monte Carlo simulations for valuation of European call and put options and implied volatilities of different stochastic volatility models including Karasinski-Sepp log-normal stochastic volatility model and Heston stochastic volatility model.

| 📊 Metric | 🔢 Value |

|---|---|

| PyPI Version |  |

| Python Versions |  |

| License |  |

| CI Status |

📈 Package Statistics

| 📊 Metric | 🔢 Value |

|---|---|

| Total Downloads | |

| Monthly | |

| Weekly | |

| GitHub Stars |  |

| GitHub Forks |  |

StochVolModels

The StochVol package provides:

- Analytics for Black-Scholes and Normal vols

- Interfaces and implementation for stochastic volatility models,

including Karasinski-Sepp log-normal SV model and Heston SV model

using analytical method with Fourier transform and Monte Carlo simulations - Visualization of model implied volatilities

For the analytic implementation of stochastic volatility models, the package provides interfaces for a generic volatility model with the following features.

- Interface for analytical pricing of vanilla options

using Fourier transform with closed-form solution for moment generating function - Interface for Monte-Carlo simulations of model dynamics

Illustrations of using package analytics for research

work is provided in top-level package my_papers

which contains computations and visualisations for several papers

Installation

Install using

pythonpip install stochvolmodels

Upgrade using

pythonpip install --upgrade stochvolmodels

Clone using

pythongit clone https://github.com/ArturSepp/StochVolModels.git

Core Dependencies

python >= 3.8numba >= 0.56.4numpy >= 1.22.4scipy >= 1.10pandas >= 2.2.0matplotlib >= 3.2.2seaborn >= 0.12.2

Optional dependencies:

qis ">=2.3.1" (for running code in my_papers)

Table of contents

- Model Interface

- Running log-normal SV pricer

- Running Heston SV pricer

- Supporting Illustrations for Public Papers

Running model calibration to sample Bitcoin options data

Implemented Stochastic Volatility models <a name="introduction"></a>

The package provides interfaces for a generic volatility model with the following features.

- Interface for analytical pricing of vanilla options using Fourier transform with closed-form solution for moment generating function

- Interface for Monte-Carlo simulations of model dynamics

- Interface for visualization of model implied volatilities

The model interface is in stochvolmodels/pricers/model_pricer.py

Log-normal stochastic volatility model <a name="logsv"></a>

The analytics for Karasinski-Sepp log-normal stochastic volatility model is based on the paper

Log-normal Stochastic Volatility Model with Quadratic Drift by Artur Sepp and Parviz Rakhmonov

The dynamics of the log-normal stochastic volatility model:

$$dS_{t}=r(t)S_{t}dt+\sigma_{t}S_{t}dW^{(0)}_{t}$$

$$d\sigma_{t}=\left(\kappa_{1} + \kappa_{2}\sigma_{t} \right)(\theta - \sigma_{t})dt+ \beta \sigma_{t}dW^{(0)}{t} + \varepsilon \sigma{t} dW^{(1)}_{t}$$

$$dI_{t}=\sigma^{2}_{t}dt$$

where $r(t)$ is the deterministic risk-free rate; $W^{(0)}_{t}$ and $W^{(1)}_t$ are uncorrelated Brownian motions, $\beta\in\mathbb{R}$ is the volatility beta which measures the sensitivity of the volatility to changes in the spot price, and $\varepsilon>0$ is the volatility of residual volatility. We denote by $\vartheta^{2}$, $\vartheta^{2}=\beta^{2}+\varepsilon^{2}$, the total instantaneous variance of the volatility process.

Implementation of Lognormal SV model is contained in

pythonstochvolmodels/pricers/logsv_pricer.py

Heston stochastic volatility model <a name="hestonsv"></a>

The dynamics of Heston stochastic volatility model:

$$dS_{t}=r(t)S_{t}dt+\sqrt{V_{t}}S_{t}dW^{(S)}_{t}$$

$$dV_{t}=\kappa (\theta - V_{t})dt+ \vartheta \sqrt{V_{t}}dW^{(V)}_{t}$$

where $W^{(S)}$ and $W^{(V)}$ are correlated Brownian motions with correlation parameter $\rho$

Implementation of Heston SV model is contained in

pythonstochvolmodels/pricers/heston_pricer.py

Running log-normal SV pricer <a name="paragraph1"></a>

Basic features are implemented in

pythonexamples/run_lognormal_sv_pricer.py

Imports:

pythonimport numpy as np import stochvolmodels as sv from stochvolmodels import LogSVPricer, LogSvParams, OptionChain

Computing model prices and vols <a name="subparagraph1"></a>

python# instance of pricer logsv_pricer = LogSVPricer() # define model params params = LogSvParams(sigma0=1.0, theta=1.0, kappa1=5.0, kappa2=5.0, beta=0.2, volvol=2.0) # 1. compute the price model_price, vol = logsv_pricer.price_vanilla(params=params, ttm=0.25, forward=1.0, strike=1.0, optiontype='C') print(f"price={model_price:0.4f}, implied vol={vol: 0.2%}") # 2. prices for slices model_prices, vols = logsv_pricer.price_slice(params=params, ttm=0.25, forward=1.0, strikes=np.array([0.9, 1.0, 1.1]), optiontypes=np.array(['P', 'C', 'C'])) print([f"{p:0.4f}, implied vol={v: 0.2%}" for p, v in zip(model_prices, vols)]) # 3. prices for option chain with uniform strikes option_chain = OptionChain.get_uniform_chain(ttms=np.array([0.083, 0.25]), ids=np.array(['1m', '3m']), strikes=np.linspace(0.9, 1.1, 3)) model_prices, vols = logsv_pricer.compute_chain_prices_with_vols(option_chain=option_chain, params=params) print(model_prices) print(vols)

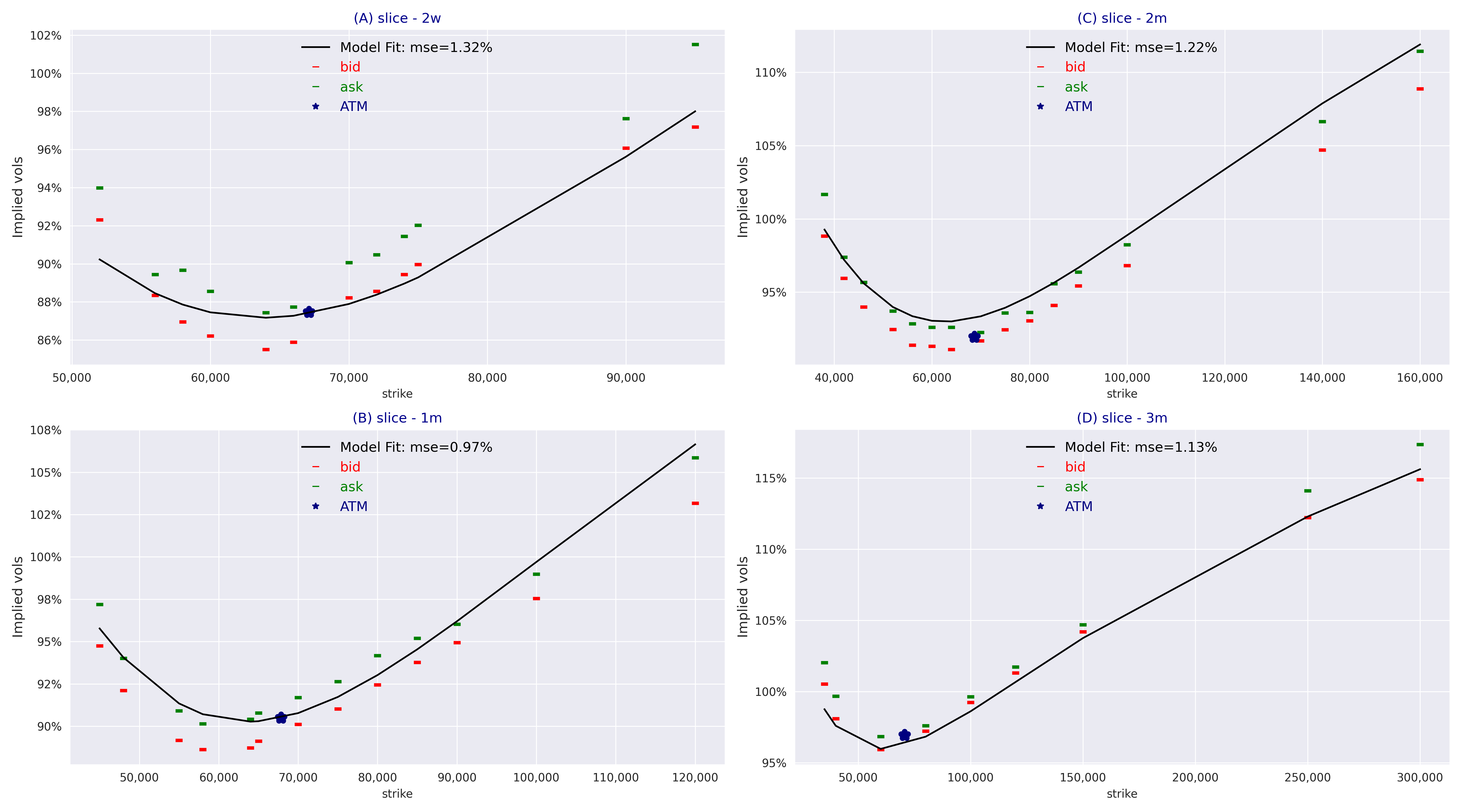

Running model calibration to sample Bitcoin options data <a name="subparagraph2"></a>

pythonbtc_option_chain = chains.get_btc_test_chain_data() params0 = LogSvParams(sigma0=0.8, theta=1.0, kappa1=5.0, kappa2=None, beta=0.15, volvol=2.0) btc_calibrated_params = logsv_pricer.calibrate_model_params_to_chain(option_chain=btc_option_chain, params0=params0, constraints_type=ConstraintsType.INVERSE_MARTINGALE) print(btc_calibrated_params) logsv_pricer.plot_model_ivols_vs_bid_ask(option_chain=btc_option_chain, params=btc_calibrated_params)

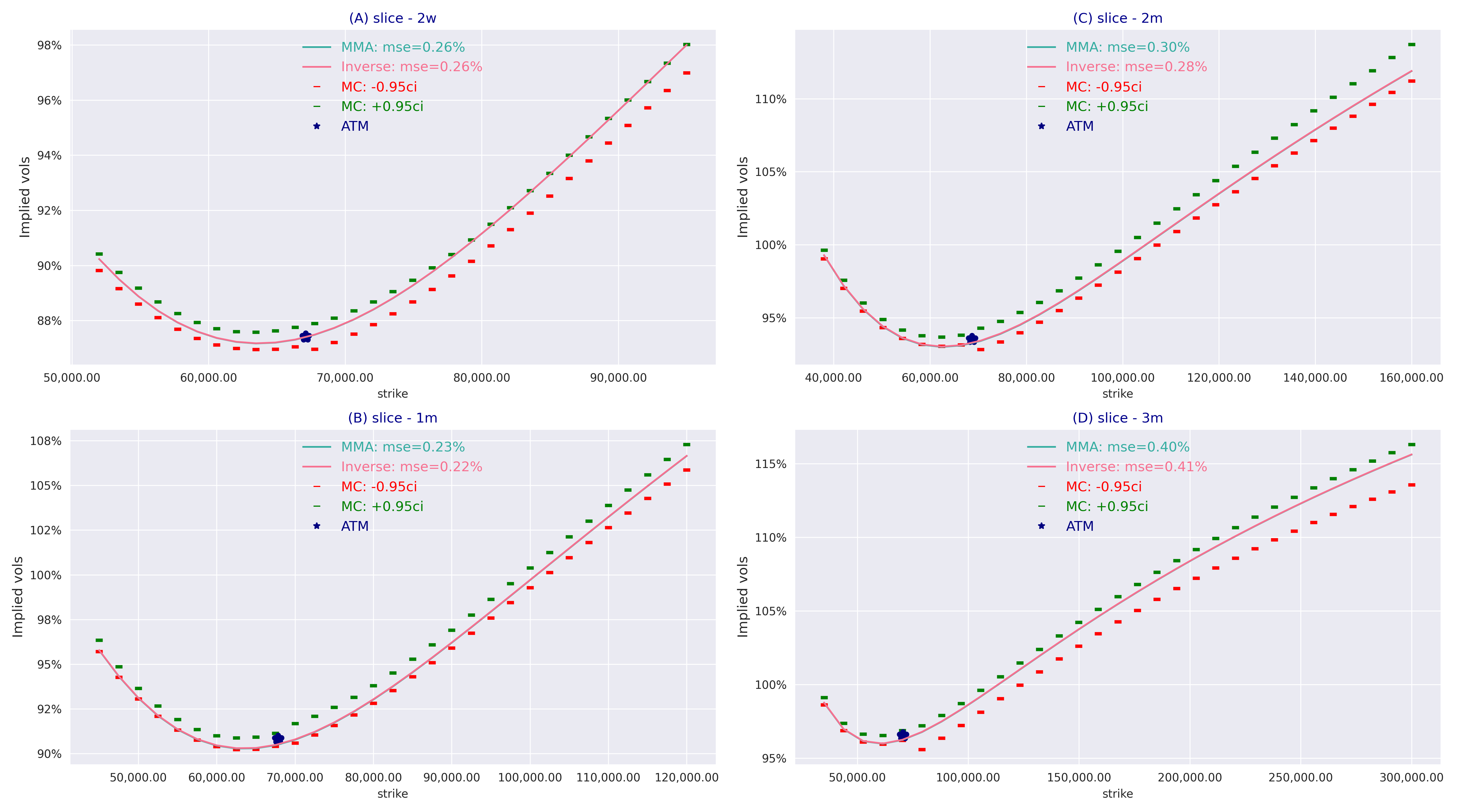

Comparison of model prices vs MC <a name="subparagraph3"></a>

pythonbtc_option_chain = chains.get_btc_test_chain_data() uniform_chain_data = OptionChain.to_uniform_strikes(obj=btc_option_chain, num_strikes=31) btc_calibrated_params = LogSvParams(sigma0=0.8327, theta=1.0139, kappa1=4.8609, kappa2=4.7940, beta=0.1988, volvol=2.3694) logsv_pricer.plot_comp_mma_inverse_options_with_mc(option_chain=uniform_chain_data, params=btc_calibrated_params, nb_path=400000)

Analysis and figures for the paper <a name="subparagraph4"></a>

All figures shown in the paper can be reproduced using py scripts in

pythonexamples/plots_for_paper

Running Heston SV pricer <a name="heston"></a>

Examples are implemented here

pythonexamples/run_heston_sv_pricer.py examples/run_heston.py

Content of run_heston.py

pythonimport numpy as np import matplotlib.pyplot as plt from stochvolmodels import HestonPricer, HestonParams, OptionChain # define parameters for bootstrap params_dict = {'rho=0.0': HestonParams(v0=0.2**2, theta=0.2**2, kappa=4.0, volvol=0.75, rho=0.0), 'rho=-0.4': HestonParams(v0=0.2**2, theta=0.2**2, kappa=4.0, volvol=0.75, rho=-0.4), 'rho=-0.8': HestonParams(v0=0.2**2, theta=0.2**2, kappa=4.0, volvol=0.75, rho=-0.8)} # get uniform slice option_chain = OptionChain.get_uniform_chain(ttms=np.array([0.25]), ids=np.array(['3m']), strikes=np.linspace(0.8, 1.15, 20)) option_slice = option_chain.get_slice(id='3m') # run pricer pricer = HestonPricer() pricer.plot_model_slices_in_params(option_slice=option_slice, params_dict=params_dict) plt.show()

Supporting Illustrations for Public Papers <a name="papers"></a>

As illustrations of different analytics, this package includes module my_papers

with codes for computations and visualisations featured in several papers

for

- "Log-normal Stochastic Volatility Model with Quadratic Drift" by Artur Sepp

and Parviz Rakhmonov: https://www.worldscientific.com/doi/10.1142/S0219024924500031

pythonstochvolmodels/my_papers/logsv_model_wtih_quadratic_drift

- "What is a robust stochastic volatility model" by Artur Sepp and Parviz Rakhmonov, SSRN:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4647027

pythonstochvolmodels/my_papers/volatility_models

- "Valuation and Hedging of Cryptocurrency Inverse Options" by Artur Sepp

and Vladimir Lucic,

SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4606748

pythonstochvolmodels/my_papers/inverse_options

- "Unified Approach for Hedging Impermanent Loss of Liquidity Provision" by

Artur Sepp, Alexander Lipton and Vladimir Lucic,

SSRN: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4887298

pythonstochvolmodels/my_papers/il_hedging

- "Stochastic Volatility for Factor Heath-Jarrow-Morton Framework" by Artur Sepp and Parviz Rakhmonov, SSRN:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4646925

pythonstochvolmodels/my_papers/sv_for_factor_hjm

Project Structure

StochVolModels/

├── stochvolmodels/

│ ├── pricers/

│ │ ├── model_pricer.py # Generic model interface

│ │ ├── logsv_pricer.py # Log-normal SV implementation

│ │ └── heston_pricer.py # Heston SV implementation

│ ├── data/

│ │ └── option_chain.py # Option chain data structures

│ └── my_papers/ # Research paper implementations

│ ├── logsv_model_with_quadratic_drift/

│ ├── volatility_models/

│ ├── inverse_options/

│ ├── il_hedging/

│ └── sv_for_factor_hjm/

├── examples/

│ ├── run_lognormal_sv_pricer.py

│ ├── run_heston_sv_pricer.py

│ ├── run_heston.py

│ └── plots_for_paper/

└── README.md

Contributing

Contributions are welcome! Please feel free to submit a Pull Request. For major changes, please open an issue first to discuss what you would like to change.

License

This project is licensed under the MIT License - see the LICENSE file for details.

Citation

If you use this package in your research, please cite the relevant papers:

bibtex@misc{sepp2024stochvolmodels, title={StochVolModels: Python Implementation of Stochastic Volatility Models}, author={Sepp, Artur}, year={2024}, howpublished={\url{https://github.com/ArturSepp/StochVolModels}}, note={Python package for pricing analytics and Monte Carlo simulations} } @article{sepprakhmonov2023, title={Log-normal stochastic volatility model with quadratic drift}, author={Sepp, Artur and Rakhmonov, Parviz}, journal={International Journal of Theoretical and Applied Finance}, volume={26}, number={8}, year={2023}, url={https://www.worldscientific.com/doi/epdf/10.1142/S0219024924500031} } @article{sepprakhmonov2023b, title={What is a robust stochastic volatility model}, author={Sepp, Artur and Rakhmonov, Parviz}, year={2023}, note={Working paper}, url={http://ssrn.com/abstract=4647027} } @article{lucicsepp2024, title={Valuation and hedging of cryptocurrency inverse options}, author={Lucic, Vladimir and Sepp, Artur}, journal={Quantitative Finance}, volume={24}, number={7}, pages={851--869}, year={2024}, url={https://www.tandfonline.com/doi/full/10.1080/14697688.2024.2364804} } @article{sepprakhmonov2024, title={Stochastic volatility for factor Heath-Jarrow-Morton framework}, author={Sepp, Artur and Rakhmonov, Parviz}, year={2025}, journal={Review of Derivatives Research}, note={Accepted}, url={http://ssrn.com/abstract=4646925} }

Acknowledgments

Special thanks to co-authors and collaborators:

- Parviz Rakhmonov

- Vladimir Lucic

- Alexander Lipton

For additional research and advanced analytics, see the companion modules and papers included in this package.

BibTeX Citations for StochVolModels (Stochastic Volatility Models) Package

If you use StochVolModels in your research, please cite it as:

bibtex@software{stochvolmodels2024, author={Sepp, Artur}, title={StochVolModels: Python implementation of pricing analytics and Monte Carlo simulations for stochastic volatility models}, year={2024}, url={https://github.com/ArturSepp/StochVolModels}, }

Contributors

Showing top 5 contributors by commit count.

Related Repositories

advimman/lama

🦙 LaMa Image Inpainting, Resolution-robust Large Mask Inpainting with Fourier Convolutions, WACV 2022

dmrschmidt/DSWaveformImage

Generate waveform images from audio files on iOS, macOS & visionOS in Swift. Native SwiftUI & UIKit views.

shibatch/sleef

SIMD Library for Evaluating Elementary Functions, vectorized libm and DFT

spatialaudio/signals-and-systems-lecture

Continuous- and Discrete-Time Signals and Systems - Theory and Computational Examples

indutny/fft.js

The fastest JS Radix-4/Radix-2 FFT implementation

psambit9791/jdsp

A Java Library for Digital Signal Processing